How an LLC can elect to be taxed like a C-Corporation with the IRS

Important notes:

1. Before changing your LLC’s tax status with the IRS, we recommend speaking with an accountant and/or a tax lawyer. There are far more things to consider than we’ve mentioned in this article.

2. The owners of an LLC are called Members. And the owners of a Corporation are called Shareholders. When an LLC elects to be taxed as a C-Corporation, in the context of discussing taxes, the owners may be referred to as Shareholders. Throughout this article, please know that the words “Members”, “Owners”, and “Shareholders” all mean the same thing.

3. Any time you see the word “Corporation”, “C-Corporation”, or “LLC/C-Corp”, please note that we are referring to an LLC being taxed as a C-Corporation.

4. For the majority of small business owners, an LLC being taxed as a C-Corporation is far less popular than an LLC being taxed as an S-Corporation (mainly because a C-Corporation has double taxation while an S-Corporation has pass-through taxation). An LLC being taxed as an S-Corporation can save an LLC owner thousands of dollars per year in self employment tax (once the LLC’s net income reaches a certain level). If you’d like more information on S-Corporation taxation, you can find that here: LLC taxed as S-Corporation.

The IRS doesn’t have a specific tax classification for LLCs. Instead, they look at how many owners – (called Members) – an LLC has to determine how the LLC will be treated for federal income tax purposes.

An LLC with 1 Member is taxed as a Disregarded Entity. Meaning, if the LLC owner is an individual person, the LLC will be taxed like a Sole Proprietorship. If the LLC owner is another company, the LLC will be taxed like a branch/division of the parent company.

An LLC with 2 or more Members is taxed as a Partnership.

Alternatively, you can ask the IRS to tax your LLC like a Corporation. There are two types of corporate taxation available for an LLC:

- An LLC taxed as a C-Corporation, or more technically known as an LLC taxed under Subchapter C of the Internal Revenue Code.

- An LLC taxed as an S-Corporation, or more technically known as an LLC taxed under Subchapter S of the Internal Revenue Code.

In this article, we will discuss an LLC being taxed as a C-Corporation.

Please note, the following sections are brief overviews and are not exhaustive. As mentioned earlier, you will need to speak with an accountant and/or tax attorney to discuss the details that are unique to your business.

Disadvantages of an LLC taxed as a C-Corp

Disadvantage: Double Taxation

This is the most commonly known disadvantage. Owners (shareholders) of an LLC/C-Corp pay taxes on two levels:

- corporate

- and individual

The LLC/C-Corp pays corporate taxes (current nominal rate is 21%) on its taxable earnings and then distributes money to its owners either by a dividend or a salary.

Either way, in addition to the LLC/C-Corp paying corporate taxes, the owners then pay taxes again at the individual level:

- A dividend is considered ordinary income and is taxed at 10% to 37%, depending on the owner’s tax bracket.

- If the owners take a salary, they pay a 15.3% self-employment tax for Social Security and Medicare (also known as FICA).

Notes:

– There are other direct means of taking money out of an LLC/C-Corp (like a loan to shareholders) and indirect means (like expenses and leases), but these are too detailed for the scope of this article.

Disadvantage: Accumulated Earnings Tax

Over time, business owners and tax professionals used different methods of avoiding double taxation, one of which is by just leaving the profits in the LLC/C-Corp’s bank account and letting the cash pile up.

To combat this, Congress passed new laws and enacted the Accumulated Earnings Tax (see IRS: Publication 542), which is a 20% tax on money that is left in the corporate bank account that is in excess of the company’s “reasonable needs”. Usually, if an LLC/C-Corp accumulates more than $250,000 in earnings (or $150,000 for Personal Service Corporations), it crosses the “reasonable” line and can trigger the 20% tax.

Note: An LLC/C-Corp that accumulates more than $250,000 (or $150,000 in a Personal Service Corporation) may be able to avoid the Accumulated Earnings Tax if they are able to prove they have a realistic plan for the use of those earnings. For example: expansion, construction, new equipment, new factory, acquisition, etc.

Disadvantage: “Zeroing out”

The other method to offset double taxation is referred to as “zeroing out” the LLC/C-Corp. This means that the LLC/C-Corp doesn’t keep earnings in the corporate bank account, and instead issues a certain percentage as dividends and the rest as salary (emptying out the corporate bank account).

So while the S-Corporation avoids corporate tax, the owners still pay ordinary income tax or self-employment tax. However, for most small business owners, they will most likely get better tax savings by having their LLC taxed as an S-Corp.

Disadvantage: Personal Service Corporations & Accumulated Earnings Tax

As mentioned above, if a Personal Service Corporation accumulates more than $150,000 in earnings, it crosses the “reasonable” line and can trigger the 20% Accumulated Earnings Tax.

The IRS considers an LLC/C-Corp to be a Personal Service Corporation if it passes both the following tests:

1. The LLC/C-Corp’s primary business activities are services offered in the following fields:

accounting, actuarial science, architecture, consulting, engineering, health, law, performing arts, or veterinary services.

2. At least 95% of the LLC/C-Corp’s stock/membership interests are directly (or indirectly) owned by employees performing the above services.

Additionally, the 95% ownership can be held by the following:

- retired employees,

- an estate of an employee,

- an estate of a retiree described above, or

- anyone who acquired the stock of the LLC/C-Corp as a result of an employee or retiree’s death

Disadvantage: Personal Holding Company Tax

The IRS considers an LLC/C-Corp to be a Personal Holding Company if it passes both the Income Test and the Stock Ownership Test.

Income Test:

60% of the LLC/C-Corp’s adjusted ordinary gross income is from passive income, such as annuities, dividends, interest, rent, and royalties.

Stock Ownership Test:

At any time during the last 1/2 of the tax year, more than 50% of the value of the LLC/C-Corp outstanding stock is owned (directly or indirectly) by (or for) 1, 2, 3, 4, or 5 people (but no more than 5 people).

Personal Holding Company Tax (20%):

The IRS imposes a 20% “Personal Holding Company Tax” on an LLC/C-Corp if it doesn’t distribute passive income earnings to its shareholders.

How did this come about?

People attempted to shelter passive income (get a reduced tax rate) via Corporations (or LLCs taxed as Corporations) because the highest corporate tax rates have been lower than individual tax brackets. The IRS eventually caught on and they weren’t big fans. Instead, the IRS wants to tax income at the highest rate possible (in this case, individual rates instead of corporate rates).

The thinking was that Corporations should be operating businesses, not scheming to shelter and reduce taxes. So Congress enacted a penalty to tax these “holding companies”. And thus the Personal Holding Company Tax was born.

Bottom line:

If you don’t distribute passive income earnings to the LLC/C-Corp shareholders, you receive an extra tax by the IRS in addition to corporate income tax.

Any income splitting strategies are rendered useless.

Disadvantage: No Personal Deductions on Corporate Losses

Unlike an LLC that is taxed as a Sole Proprietorship or a Partnership where the owners can offset their taxable income by writing off business expenses, an LLC/C-Corp can’t do this.

Instead, corporate losses can only be used to offset the taxable income on the corporate tax return (Form 1120), not to offset the taxable income on the owners’ personal tax return (Form 1040).

Disadvantage: Capital Gains Tax

Corporate capital gains tax rates may be higher than personal capital gains tax rates.

Unlike individuals, which pay different capital gains tax based on whether an asset is held for more than a year or less than a year, LLC/C-Corps cannot classify their capital gains tax.

Earnings from the sale of an asset are taxed at the corporate tax rate.

For that reason, a pass-through entity (LLC taxed as Sole Proprietorship, Partnership, or S-Corporation) may be more beneficial for capital gains tax since they are taxed at personal rates, not corporate rates.

Disadvantage: Reverting from C-Corp Tax Qualification Back to Default Tax Classification

Converting your LLC taxation from a C-Corp back to its default status (Sole Proprietorship taxation or Partnership taxation) will likely have tax consequences. Even though you are only changing the tax classification of the LLC, the IRS treats this action like you’re liquidating the company and as a result, there will be a tax liability.

Disadvantage: Registering with the U.S. SEC

This isn’t really a “disadvantage” because if you’re registering with the SEC, it’s in the hope that you will soon be raising more capital; however, we wanted to mention it since it is an extra step.

An LLC/C-Corp is required to register with the U.S. Securities and Exchange Commission (SEC) if it has over 500 shareholders and more than $10 million in assets.

Disadvantage: Strict Record Keeping Requirements

LLC/C-Corps must maintain more corporate and financial records than that of pass-through LLCs (LLCs taxed as Sole Proprietorships, Partnerships, or S-Corporations).

Advantages of an LLC taxed as a C-Corp

Note: Many of the advantages listed below are for companies looking to raise substantial capital and/or go public. In many cases, it may be more beneficial to have the state entity be a Corporation instead of an LLC that elects C-Corporation tax treatment by the IRS. If this is applicable to you, we strongly recommend having a conversation with your legal and tax advisors.

Advantage: Unlimited Number of Owners (Shareholders)

Unlike an S-Corporation which is limited to 100 shareholders, an LLC taxed as a C-Corporation is allowed to have an unlimited number of shareholders. This is beneficial for companies looking to raise money and/or go public.

Additionally there is more acceptance in the capital marketplace (venture capital, angel investors, etc.) towards the issuance of shares vs. the issuance of LLC membership interest.

Advantage: No restrictions on who can hold shares

Unlike an S-Corporation which has restrictions on its shareholders (ex: non-US residents), an LLC taxed as a C-Corporation faces no restrictions on who can own shares in the company.

This is also beneficial for companies looking to raise money and/or go public.

(related article: can a foreigner own an S-Corporation?)

Advantage: Raising Money and Going Public

For the reasons mentioned above, if you’re looking to raise a lot of capital and/or take your company public, a Corporation (or an LLC taxed as a C-Corporation) is often the best choice.

Advantage: Widest Range of Tax Deductions

For businesses with a large number of applicable write-offs (see fringe benefits below), C-Corporation taxation has the widest range of tax deductions.

Advantage: Ease of Stock Transfers

Transferring stock/ownership in a C-Corporation is often far easier than transferring LLC membership interests/stock in a pass-through LLC, such as an LLC taxed as a Sole Proprietorship, Partnership, or S-Corporation.

Advantage: Qualified Small Business Stock

As per Section 1202 of the IRS Code, C-Corporations can get a reduced capital gains tax on Qualified Small Business Stock, aka QSBS.

Advantage: Healthcare Fringe Benefits

Health insurance premiums can be written off as a business expense of the C-Corporation. And while you can do the same thing in an S-Corporation, the write-off actually shows back up on your personal tax return as a form of taxable income (if you own 2% or more of the S-Corporation).

Besides the health insurance premiums, there are a number of other healthcare benefits and preferential treatment that C-Corporations receive.

Some examples include write-offs on disability insurance, life insurance, health savings plans, dental care, eye care, and accident plans.

There are far more details and restrictions (such as the need to provide fringe benefits to 70% of their employees, for example) that apply to C-Corporations, but these are in-depth conversations that you’ll need to have with your tax professional.

Advantage: Other Benefits

Besides the information listed above, there may be other tax benefits of an LLC being taxed as a Corporation and they should be discussed with your tax professional.

Other tax benefits include retirement plans, gym memberships, meals provided at work, gift certificates, cash, and other rewards for employee achievement, education assistance, company-owned vehicles, public transportation for employees, and moving and housing benefits.

Consider a Corporation instead of an LLC taxed as a C-Corporation

If you are considering having your LLC taxed as a C-Corporation, we recommend speaking with an accountant and/or business lawyer to see if simply forming a Corporation (which is automatically taxed as a C-Corporation) is more beneficial.

State-Level Corporate Taxes

It’s important to keep in mind that everything above is written generally and is in the context of federal taxes.

There are currently more than 40 states which charge corporate income taxes.

Another important thing to note is that a handful of states (Alabama, Iowa, Louisiana, and Missouri) allow for LLCs taxed as C-Corporations to deduct a percentage of their federal taxes, which therefore reduces the LLC’s effective state income tax rate. (source)

Local and Municipal Corporate Taxes

In addition to paying taxes at the federal-level and the state-level, many LLCs taxed as C-Corporations also have to pay taxes with their local government or municipality.

For example, this means corporate taxes may need to be paid to your county, city, township, or borough; or all, or none of the above.

Your LLC’s requirement will be determined by where you do business and you’ll need to speak with your accountant regarding the details.

Additional Taxes

Furthermore, in addition to the 3 primary levels of income tax (federal, state, and local), LLCs and their owners may be subject to additional taxes based on their industry and whether or not they have employees.

Some examples include payroll tax, federal unemployment tax, state unemployment tax, workers’ compensation tax/insurance, capital gains tax, state franchise tax, gross receipts tax, dividend tax, sales tax, use tax, excise tax, and more.

Takeaway

Electing C-Corporation tax status for an LLC generally makes sense if your company is looking to raise money, go public, or has large healthcare expenses.

There may be other benefits to certain types and sizes of businesses, but determining those is a conversation you’ll need to have with your tax accountant.

What do most people do?

Most of our readers are just starting out, so they leave their LLC in its default tax status (Sole Proprietorship or Partnership taxation) until their business becomes more profitable.

Then years down the road, the owners, after speaking with a tax professional, may consider having their LLC taxed as an S-Corp in order to save money on self-employment taxes.

Still want to elect C-Corp tax classification for your LLC?

If you still decide to have your LLC taxed as a C-Corp, you will find the instructions listed below.

Form 8832 for C-Corporation election

Form 8832 is used for an LLC that wants to elect federal tax treatment as a C-Corporation.

IRS: About Form 8832, Entity Classification Election

IRS: Download Form 8832 PDF (see page 4 for instructions)

Important: The information below is a general overview. It’s important to note that there are serious consequences for electing the incorrect tax classification for your LLC. We strongly recommend discussing and reviewing Form 8832 with your tax professional before electing C-Corporation status for your LLC.

At the top of the form:

Enter your LLC name, EIN, and address. Check any applicable boxes to the right of “Check if”.

1.) Type of election:

If you just formed your LLC, select “a” (“Initial classification by a newly-formed entity. Skip lines 2a and 2b and go to line 3“).

If your LLC was already in existence, select “b” (“Change in current classification. Go to line 2a“).

2a.) Has the eligible entity previously filed an entity election that had an effective date within the last 60 months?

Newly-formed LLCs should skip 2a.

If you selected “b” in #1, let the IRS know if you made an entity election that had an effective date within the last 5 years.

2b.) Was the eligible entity’s prior election an initial classification election by a newly formed entity that was effective on the date of formation?

Newly-formed LLCs should skip 2b.

If you selected “Yes” in #2a, let the IRS know if this classification election was made at the time the entity was formed.

3.) Does the eligible entity have more than one owner?

A pretty straightforward question. Answer accordingly.

4.) If the eligible entity has only one owner, provide the following information:

If your LLC has 2 or more Members (owners), skip #4.

If your LLC has 1 Member (owner), enter the owner’s legal name in “a” and their Taxpayer ID Number, such as a person’s SSN or ITIN or an entity’s EIN Number.

5.) If the eligible entity is owned by one or more affiliated corporations that file a consolidated return, provide the name and employer identification number of the parent corporation:

If your LLC is owned by another company (that files a consolidated return) enter the name of the parent company and its EIN Number.

6.) Type of entity

This is where you will elect C-Corporation tax treatment for your LLC.

The applicable check box is “A domestic eligible entity electing to be classified as an association taxable as a corporation.”

7.) If the eligible entity is created or organized in a foreign jurisdiction, provide the foreign country of organization:

If your LLC is formed or organized outside of the U.S., enter the country in which your LLC was formed.

This is not applicable to the majority of our readers since most of them form LLCs in the U.S.

8.) Election is to be effective beginning (month, day, year):

Enter the month, day, and year that your C-Corporation tax election will take place.

Make sure to speak with your accountant about when you should make your C-Corporation election go into effect.

And if you are filing a C-Corp tax election past the deadline, you’ll want assistance from your tax professional about what to enter on page 3 of Form 8832 (Section II – Late Election Relief).

For more information, please see the “When to File” section inside the instructions for Form 8832.

9.) Name and title of contact person whom the IRS may call for more information:

Enter your name and title (ex: “Member”) in #9.

10.) Contact person’s telephone number:

Enter a good phone number where the IRS can reach you in case they have any questions.

Consent Statement and Signature(s):

Sign the form, enter today’s date, and enter your title to the right.

11.) Provide the explanation as to why the entity classification election was not filed on time:

If you are making a late election, your explanation will go here. If you are filing on time, you don’t have to worry about this section.

Make a copy of Form 8832 before sending to the IRS

After you properly fill out and sign Form 8832, make a copy (or a few to be safe) and keep them with your LLC’s records.

It’s important to make a copy before sending 8832 to the IRS because you’ll need to include a copy of 8832 with your upcoming federal tax return.

How to send Form 8832 to the IRS

You’ll need to mail the completed and signed Form 8832 to the IRS.

The mailing address you should use will be determined by where your LLC is located.

Please reference the “Where To File” section in the instructions of Form 8832. Make sure to reference that information with the addresses listed below.

If your LLC is located in Connecticut, Delaware, District of Columbia, Georgia, Illinois, Indiana,Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Vermont, Virginia, West Virginia, or Wisconsin:

Mail to:

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999

OR

If your LLC is located in Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Tennessee, Texas, Utah, Washington, or Wyoming:

Mail to:

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201

Important: When filing your LLC’s federal tax or information return (for the year matching your LLC’s C-Corp election), make sure to include a copy of Form 8832. If your LLC doesn’t have to file a return for that year, a copy of Form 8832 must be included with the LLC owner’s tax return. If you forget to do this, you won’t lose your LLC’s C-Corp tax election, but the IRS may assess penalties.

How long is approval for an LLC taxed as a C-Corp?

It generally takes about 6 to 8 weeks before the IRS will mail you back a confirmation of your LLC’s new tax status.

The IRS will send you back an approval (or rejection) to the address you list at the top of Form 8832.

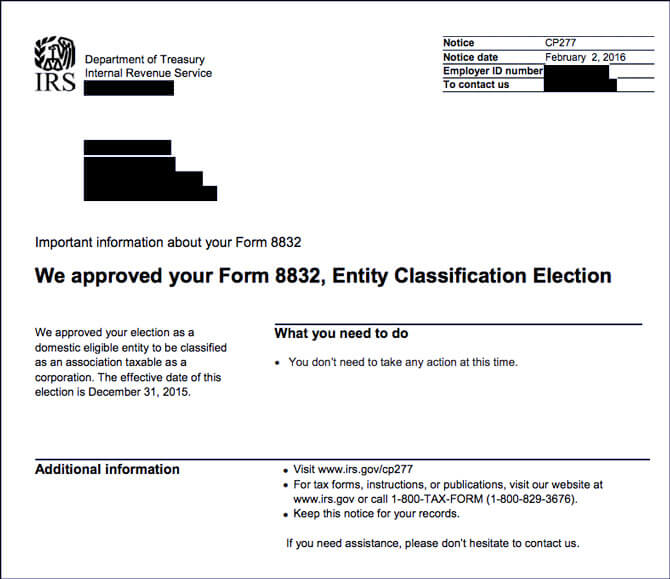

If your tax election status is accepted, the IRS will send you an Approval Letter, also known as Notice CP277.

Here’s an example of what it will look like:

If after 75 days, you haven’t received anything back from the IRS, you can call them at 1-800-829-0115 to check the status of your LLC’s C-Corp tax election.

Need a copy of your LLC taxed as a C-Corp approval letter?

If you’ve already filed Form 8832 for your LLC and you’ve received C-Corporation tax status, but you lost your Confirmation Letter (Notice CP277), you’ll need to call the IRS at 1-800-829-4933 for another confirmation letter.

Is Payroll needed for my LLC taxed as a C-Corporation?

You don’t have to be an employee in a C-Corporation. However, if you (or other owners) will be an employee of the Corporation, then yes, you’ll need to take payroll.

That means filing:

- Federal Forms 941 (quarterly) and 940 (annually)

- Annual Federal W-3 and W-2(s)

- State W-3 and W-2s (if applicable)

- State Unemployment returns (quarterly)

- State withholding tax (if applicable)

If you need a good payroll service, we recommend Gusto Payroll.

Form 8832 Can also Revert Your Tax Status

It’s important to note that Form 8832 is not only for LLCs that want to be taxed as Corporations, but it’s also for LLCs currently being taxed as Corporations that want to revert back to an LLC’s default tax classification.

Meaning:

A Single-Member LLC currently taxed as a C-Corporation can file Form 8832 and revert back to being taxed as a Sole Proprietorship.

A Multi-Member LLC currently taxed as a C-Corporation can file Form 8832 and revert back to being taxed as a Partnership.

Form 8832 can’t be used to revert from S-Corp status to default status

Unlike Form 8832, which can be used to revert an LLC being taxed as a C-Corporation to its default tax classification, Form 8832 cannot be used to revert an LLC being taxed as an S-Corporation to its default tax classification.

In fact, there is no “official” IRS form to revert an LLC taxed as an S-Corporation to its default tax classification. Instead, you’ll need to mail a letter to the IRS manually requesting the change in tax classification. The IRS will write back in 30-60 days with confirmation and then you’ll be able to go back to filing taxes for your LLC in its default tax classification.

If you have an LLC taxed as an S-Corporation and you’d like to revert to default tax classification, you can find instructions here: LLC revoking S-Corporation election.

References

IRS: Tax Brackets

IRS: S-Corporations

26 US Code Section 11

26 US Code Section 531

26 US Code Section 535

26 US Code Section 543

26 US Code Section 561

26 US Code Section 541

IRS: About Form 8832

IRS: About Form 1099-DIV

IRS: Instructions for Schedule D

IRS: Instructions for Form 1120

IRS: Section 9, Notices and Codes

IRS: Publication 542: Corporations

IRS: About Schedule PH (Form 1120)

IRS: FAQ about personal corporations

IRS: Understanding your CP277 Notice

IRS: Publication 3402: Taxation of LLCs

IRS: Instructions for Schedule PH (Form 1120)

IRS: Publication 583: Starting a Business and Keeping Records

26 US Code, Subchapter C – Corporate Distributions and Adjustments

IRS: Notice of Potential Qualification as Personal Service Corporation

IRS: CP224 example – You may qualify as a Personal Service Corporation

Matt holds a Bachelor's Degree in business from Drexel University with a concentration in business law. He performs extensive research and analysis to convert state laws into simple instructions anyone can follow to form their LLC - all for free! Read more about Matt Horwitz and LLC University.

I’ve got a GENERAL question about retained earnings and the Accumulated Earnings Tax. Nobody seems to like to discuss this topic, which I suspect is why the “double-taxation” thing is always one of the top few stated drawbacks of C-Corp taxations. I’ve had lots of people tell me that a Corp can invest in anything a person can, and vice-versa. It’s just that the Corp needs a Resolution written up that outlines the intention behind some future action or investment along with the expected requirements and capital to accumulate over time. Also, since it’s usually a longer-term strategy, it’s subject to shifts in the market that can cause it to be subject to periodic reviews and alterations.

Let’s say you have a goal to buy a rental property in Breckenridge, CO, that could eventually become a remote office, and you’d like to pay cash for it.

Your options are to buy it: (1) through your Corp; or (2) personally. (Probably within a separate LLC or Trust).

Current statistics show that (as I write this), a reasonable amount of funds needed to buy a property in Breckenridge is in the $1.2M to $1.7M range. So if your goal was to pay cash, you’d need to be able to accumulate this amount first.

For the Corp to buy this, the income taxes on the earnings are currently 21%. But if you have a pass-thru entity, then they’d be at a far higher rate (assuming a mid-6-figure annual income).

Is there any particular reason NOT to buy it through the Corp? As long as you have a proper Resolution outlining this goal, is the IRS going to question the accumulation of funds for it? — Just GENERALLY SPEAKING?

In GENERAL … are you going to need to have something like a detailed 250-page project planning document to justify building up $1.5M for a future purchase? Or would a fairly simple Resolution be sufficient? Or are the cards stacked against this kind of thing?

Hi David, great questions, and I wish I knew the answer, but this is beyond the scope of work we run into. I’d recommend speaking with a corporate accountant or two. Thanks for your understanding.

Can’t the dividends be counted as qualified dividends for the owner of the LLC taxed as a C-Corp?

Hi Daniel, we don’t get too far into the weeds with LLCs taxed as C-Corps, so I’m not sure. You’ll need to check with an accountant. Thank you for your understanding.

Hi Matt,

We are 1-10 international citizens and non-US residents. We want to invest in real estate mainly raw land and trade it after holding it between 6 months to 3 years. Each land parcel will be in different LLC. What would be the best struture? Will it be a Delaware LLC or LLC as C-Corp. We will not de drawing any salary from the LLC or put expenses in it. Also, there would be 15% withholding tax once the land parcel is sold. How will the profits be taxed in US?

Great info on your site, Would appreciate your feedback. Thanks

Hi Ron, there isn’t a simple answer here, as it depends on a number of factors. We recommend you work with an accountant to dive into the specifics of your situation. Thanks for your understanding.

I have an LLC. This is a startup company and eventually I will be looking for investors. Should I change my company and incorporate or elect to be taxed as a C-Corp and still solicit investors as a stock company. Seems like just changing the company to a corporation makes the most sense.

Hi Terry, in the context of how things are done in Silicon Valley, most investors prefer a Delaware C-Corporation, not an LLC taxed like a C-Corporation.

I filed a new LLC in California in January and want to be taxed as an C-Corp. I filled out form 8832, but it appears I have to send in a copy of my personal taxes with it to file for this classification. Is there any way around this, I’m not trying to conflate the two. I want it to be its own entity. Not attached to my personal taxes whatsoever. Plus I formed the LLC after the beginning the year(2021) and don’t owe taxes for this entity until next year.

Hi Andrew, apologies, but we’re not familiar with this being a requirement. Form 8832 is for a federal tax election, but Assembly Bill 85 affecting California LLCs is about state franchise tax.

Thank you for the reply! Much appreciated.

Good Morning Matt,

We have talked a few times in the past.

Is LLC electing to be taxed as a C Corporation subject to IRC 351 (The transferee must attach a statement to its tax return for the year in which the exchange took place, including a description ofproperty, liabilities, and the stock and property transferred in the exchange)? I don’t think so because it is not a change in legal entity only tax entity.

Sincerely,

Justin Botillier

Hi Justin, I hope you’re well. We are not sure about this. Thank you for bringing it to our attention.

I found this:

https://www.law.cornell.edu/cfr/text/26/301.7701-3

& this:

https://www.law.cornell.edu/cfr/text/26/1.351-3

I am not sure that they actually apply, however I would be interested in your feedback.

Thank you Justin. We are not sure about this. We recommend reaching out to another CPA. Thank you for your understanding.

Hi Matt, thank you for putting so much info in the article. I am currently live in Las Vegas, Nevada and thinking about forming an LLC taxed as C Corp. My question is , can I request the LLC to be taxed as C corps two months after I form the LLC. Thanks.

Hi Ben, you’re very welcome. Yes, you can make the C-Corp election for your LLC at any time. There is no “deadline”. Hope that helps.

We have a MMLLC that after a number of years has elected to be a C-corp. For the year of conversion, we file a 1065 to the date of conversion then a 1120 for the remaining months of the year. Is the 1065 a final return and is the 1120 an initial return?

Thank you.

Hi Nancy, we’re not allowed to comment on specifics regarding tax forms. You’ll want to run it by another accountant. At quick glance though, it sounds correct. Hope that helps.

Wanna change my LLC. to a C-Corp

Hi Harold, do you want to convert your LLC to a Corporation at the state level? Or do you want to keep your LLC at the state level, but have the IRS tax your LLC like a C-Corporation? Is there already activity and history in your LLC, or is it brand new? What is the reason you’d like to change?

Hi Matt,

I have set up a single-member LLC in the state of California. I have read from various sources that single-member LLC owners can pay themselves W-2 wages. Then when tax time comes, the LLC can deduct those wages on the owner’s Schedule C and the owner will report those wages on his 1040. But I have also read that this accounting treatment is not allowed for tax filing purposes. Instead, the owner should take distributions or guaranteed payments from the LLC unless the company elects to be taxed as an S-Corp, in which case the owner can treat himself as an employee of the company and receive W-2 wages.

My question is, can I put myself on payroll and receive W-2 wages (both from a legal and tax standpoint) from my single-member LLC.

Much appreciated!

Hi Colin, you’re correct. A Single-Member LLC taxed in default status (taxed as Sole Proprietorship) cannot take a W-2 salary as you are deemed self-employed.

Hi Matt,

I set up an LLC owned by my self directed IRA. I want to elect to have the LLC be taxed as a C-corporation to optimize investment in activities that would incur UBIT (Unrelated Business Income Tax).

I have a question related to filling out Form 8832. Part I #4.

The name of the owner in 4a will be my IRA.

What should I use as the identifying number of owner in 4B? Should it be my personal SSN, or should it be the EIN of the custodian of my self-directed IRA? Technically the owner of the LLC is my IRA, but is the IRA considered a disregarded entity?

In the instructions for Form 8832, it states: If the electing eligible entity is owned by an entity that is a disregarded entity or by an entity that is a member of a series of tiered disregarded entities, identify the first entity (the entity closest to the electing eligible entity) that is not a disregarded entity.

Thanks,

Sky

Hi Sky, thanks for reaching out. Apologies, but we’re not sure about this.

Great site!

I am a non US citizen not living in the US.

I have recently had a LLC registered on my behalf in the state of Wyoming and I need to get an EIN for the LLC.

I understand that a LLC is viewed as a disregarded entity by default by the IRS but that as a non US citizen I can select to have it taxed as a C-Corporation.

I would appreciate your advice on whether I should leave the taxation of it as is (disregarded entity) or whether I should select that it be taxed as a C-Corporation.

Here is some additional information that may be relevant:

As previously stated, my LLC is registered in Wyoming and I am a non US citizen not living in the USA. I am the only member. I will be selling products under my own brand that are manufactured in the US and at least 90% of my sales will be to US consumers (direct or via sales platforms such as Facebook) or via retail brick and mortar stores.

I will not require a warehouse or employees as the manufacturer will drop ship the items directly to my customers.

I must be able to pull money (profits) from the business (call it management fee or something similar) to my home country.

For EIN purposes, should I leave the tax status of my LLC as is (default option) or elect to be taxed as a C-Corporation?

Your advise will be greatly appreciated. Many thanks in advance!

Thanks Casper! Regarding your U.S. LLC being disregarded or being taxed as a C-Corporation, you’ll need to speak to an accountant. We recommend working with an accountant that specializes in filing non-US resident taxes. We don’t have any recommendations at this time. Here are some additional resources on our site: how to get an LLC EIN without SSN and IRS Form 5472 for foreign-owned Single-Member LLC. Hope that helps!